By Kathryn Hazelett

Are you prepared to jump into retirement? Do you anticipate a soft landing or does it feel more like jumping off of a cliff without a parachute? For the majority of Arkansans and Mississipians (as well as the majority of Americans), it likely feels like the latter.

If you are over age 65, your parachute is likely in the form of a pension that is stitched together with Social Security benefits. If you entered the workforce in the 1960’s or 1970’s, it’s likely that your employer offered what is called a pension or defined-benefit plan, which guarantees a specific benefit or payout upon retirement.And, because of this benefit structure (a certain amount each month), you are more likelyto have a retirement parachute to ease you into a soft landing for retirement.

For the rest of us, we’re looking at a much bumpier landing without some significant changes – from both the public and private sector. What those changes look like is up for debate, but retirement scholars generally agree that we need the following four A’s to ensure that retirement opportunities exist for everyone. This report provides insight into each “A” as well as look into what is being done in other parts of the country to help make our landing as smooth as possible.

The Four A’s of Retirement

- Access to a Retirement Plan

- Automatic Enrollment in a Plan

- Automatic Investment of Retirement Savings

- Automatic Escalation Savings Over Time

******************************************************************************************************

Between 2000 and 2014, according to the Stanford Center on Longevity’s Sightlines Project, the levels of financial security have dropped for every age group under the age of 65. One of the factors in that decline is a lack of access to employer-sponsored retirement plans.

In Mississippi, 45% of employees do not have access to a workplace retirement plan, but when employees do have that access, 84% participate. In Arkansas, the percentages are similar (45% have no access, while participation rates are at 82%). It would appear from just this snapshot that access to a workplace plan makes a big difference in whether or not people save for retirement. And, indeed access is one factorin retirement savings.

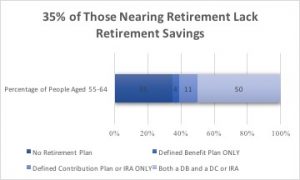

But, access itself does not guarantee a parachute or a soft landing. Retirement coverage, or access to any type of retirement plan, for those nearing retirement age (those between the ages of 55 and 64) is pretty dismal.

Will We Retire?

Given the low rates of access to workplace retirement plans and the low rates of savings for those nearing retirement age[1], a reasonable question to ask is whether workers are actually retiring. Surprisingly the answer, at least so far, is yes. The average retirement agein Arkansas is 62 and in Mississippi, it’s 63. Will we still be retiring at these ages in ten years?

National data does already show an increase in workforce participation for those over 65. Between 2000 and 2012, the percentage of those remaining in the workforce (at least part time) has increased26% for those between 65 and 69 and has increased 42% for those workers between the ages of 70 and 74. What’s interesting about these increases is that they are almost wholly from those with greater educational attainment, perhaps indicating the decision to continue working was due to social or life satisfaction considerations or due to the white-collar nature of the jobs, but that is certainly not true of all workers.

Indeed, AARP recently analyzedthe results of the 2017 retirement confidence survey and they found that 39%of workers plan to work during retirement just to make ends meet. That is well over one-third of all workers nearing retirement age.

We will need to pay close attention to changes in the retirement age in the coming years and we will need to ask questions about why those nearing or past the traditional retirement age of 65 may or may not remain in the workforce. The current data is incomplete, but it appears that we are facing a shift upwards in retirement age; will that shift primarily be because people are choosing to work longer for social reasons or will it be that people have to work longer to make ends meet? Paying close attention to this data now will help us better direct policy solutions in the near future.

Will We Face Downward Economic Mobility?

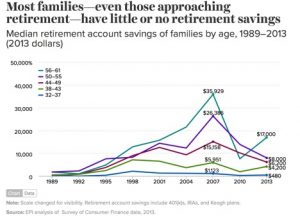

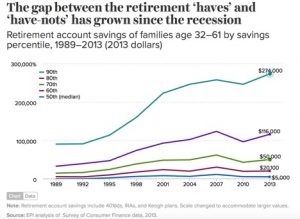

As of today, we’re retiring, but many of us are downwardly mobile in retirement due to insufficient savings. If we look at retirement savings data in a bit of a different way, we can see that every income group has underfunded retirement needs, which leads to that downward mobility.

What’s startling, though, is that while every income group is facing downward mobility, those at the bottom of the economic ladder are facing a much deeper crisis.

Inequity in Measuring How Much We Need to Retire

A common rule of thumbwhen calculating how much to save for retirement is that you will need to have 85% of your current (last) income to maintain your standard of living. While this is a good way for some to estimate, it doesn’t account for differences in wealth or assets; it leaves out the fact that retirees at different points on the income ladder are facing drastically different situations. If a family is already struggling to make ends meet at 100% of income, it is then obvious that that same family will be much worse off at 85% of their income. One way to look deeper at this issue of measuring how much we need to retire is to consider a family with a house whose mortgage is paid off compared to a family who has always rented.

The family who owns their home will not have to factor in continued mortgage payments as part of their monthly retirement costs. Not only will they not have the monthly payment, they also have equity in their home (it has a cash value if they decided to sell or downsize). This family’s future looks a lot different than that of the family who has always rented. Not only do they have to factor in a continuing rental payment each month, they also lack the equity that many homeowners rely on when retiring. These differences in wealth are not anecdotal; the data bears them out.

And, wealth disparities(and retirement plan participation and savings amounts) are heightened for blackand Hispanic families. The datashows that the “racial wealth gap is primarily a housing wealth gap.”[2]

Retirement also looks different for those entering retirement without a spouse who has also saved. With only one retirement savings plan to rely on, single people also face significantly different situations that those who have two savings plans.

If we’re retiring today with unmet retirement needs (some much more entrenched than others) and we’re facing downward economic mobility, what will the picture look like in twenty years? A lot bleaker with very few parachutes, unless we make some changes.

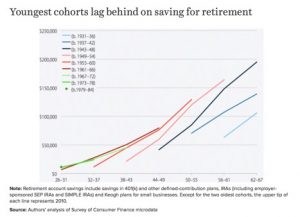

Remember when we mentioned that levels of financial security have dropped for everyone under 65? It’s especially bleak for our youngest workers.

And, for retirement specifically, we aren’t saving. The data for Arkansas and Mississippishow that even when there is access to a retirement plan, younger workers participate at a lower rate.

While it’s true that our youngest workers do have more time to save for retirement, it is also true that when we don’t start saving early, we are going to have to save a lot more later in life to have enough for retirement, especially given the structural changes in our parachutes.

How Did We Get Here?

But, before we leap forward and look at the potential to retire in 20 or 30 years, we need to look back to see how the holes in our parachutes appeared and widened. The history is important.

Until the 80’s the retirement parachute was a pension and social security. In the 80’s, the 401(k) was introduced; it was originally supposed to be a supplement to pensions, but instead, employers (anxious to reduce costs) switched from offering a pension to offering ONLY a 401(k). Pensions had also helped to level the retirement field for women and minorities.[3]

Now, let’s leap to 2015 when just 5% of employers are still offering pensions to new employees. This shift to an employee-focused retirement and away from an employer-focused retirement means the onus to save rests almost solely with employees; there is no longer a guaranteed payout at retirement. The amount you save isthe amount that you have for retirement.

And, this system works against human nature. When we start our careers, we are not thinking about saving for retirement; we are buying cars and saving for a house, and likely paying our student loans and for childcare for our kids. So, we are NOT taking advantage of the greatest force in savings: TIME.

As we know when we pay our credit card bills, the power of compound interest is mighty. When we save, that power works for us – small investments add up over time. We are better off saving when we start out.

Put in number terms, every dollar NOT saved in our 20s requires 3 or 5 dollars in our 50s and 60sjust to make up the difference….the power of compound interest IS mighty.

What can we do? The retirement system is stacked against us; our parachutes are either filled with holes or non-existent as we face retirement. The at-hand solutions seem to be to save more and earlier or to work longer.

While we did see that some older workers are choosing to stay in the workforce and while it is safe to assume that those increases will continue, for many workers, that’s not an option. For some, physical and mental limitations prevent them from continuing to work and for everyone, job availability depends upon a capricious labor market. For many older workers, the hours and wages available are not sufficient to make ends meet. Working into old age should also not be a requirement in order to avoid living in poverty.

How Can We Increase Access and Savings?

We have to save and sew our own parachutes, but how?

As mentioned earlier, many of us do not have access to a workplace retirement account. For those of us who do, we’re not participating. And, even if we are participating, we are not saving enough.

Creating our new parachute will require four things:

- Access to a retirement plan

- Automatic enrollment in that plan

- Automatic investment of retirement savings

- Automatic escalation of the amount or percentage of savings over time

In other words, we have to make it EASY. For non-wealthy workers, savings for retirement is going to happen at the workplace, so every worker should have access to a retirement plan at work (#1 and 3). And, once access is in place, behavioral economics also tells us that when we don’t see it, we don’t spend it(#s 2 and 4).

For any employee with a workplace retirement account, these four panels of a parachute would be stitched together like this: an employee starts a new job, she is automatically enrolled into the employer-sponsored retirement plan. She could opt-out, but she knows she needs to save and this makes it easier. She is also glad that the complicated investment decisions (how her savings will actually grow over time) will be tackled by the plan’s organizer. Again, it would be possible for her to do this, but she trusts that her savings will grow and she was asked questions about how much risk she feels comfortable with as well as her age and how long she anticipates working. And, last but not least, she is signed up for automatic escalation. In other words, when she gets a raise, a portion of that raise goes directly to her retirement account, while the rest goes into her bank account.

In order for all employees to have this kind of access, we have to make it less of a hurdle for employers, especially small employers, to offer a retirement plan. (In Arkansas and Mississippi, access to a workplace plan is right at or less than 33% for employers with fewer than 50 employees and is right at or less than 22% for employers with fewer than 10 employees. And, in both states, those employees make up 28% of the workforce.)

In addition, employers that already offer a retirement plan can consider automatically enrolling new employees unless they opt out. Employers can also include information on automatic escalation in their orientation. Some academicsare also proposing solutions.

How Can States Help?

As is often the case when the federal government does not offer a solution, state governments step up and innovate. That is just what is happening today; states are stepping up and enacting policies so that it is easier for employers to offer a retirement plan and therefore easier to stitch together our parachutes[4].

As you can see, state innovations can take one of several shapes. States can:

- Facilitate a marketplace for small employers to seek retirement plans,

- Start a publicly-administered direct contribution plan,

- Create an auto-IRA, or

- Develop a hybrid model

Whichever choice a state makes, the size of these state plans allows for low fees, diversified investments, and the feasibility of annuities, which is a key component of ensuring payments for the lifetime of the retiree, and takes us closer to the pensions seen prior to the 80s.

What are the major differences in state’s choices? Due to some federal laws regarding retirement plans, the auto-IRA’s do not allow employer contributions, but they can include auto-enrollment and auto-escalation. The others allow employer contributions and also can include auto-enrollment and auto-escalation. Being able to take advantage of a matching contribution by an employer is a very positive savings mechanism for employees, but as we have seen, having access to a plan with auto-enrollment and auto-escalation is critical.

These last two components are key to any retirement plan. When we are automatically enrolled in a retirement plan with the option to opt-out, we stay in the plan and therefore we save for retirement! Automatically being opted-in to the program makes it easy to save. In fact, the opt out rates are only around 10%.But, as we know, simply having access is just one step. We also have to have an auto-investment option, which is covered in these state innovations, and we have to have auto-escalation, which means our savings rates have to go up as we earn more money. That last aspect is a key point. If we are expecting a raise or cost of living increase and part of it automatically goes into our retirement savings, we don’t miss the money. As a behavioral economist would put it, it “diminishes our loss aversion.” Including auto-escalation improves savings.

We have parachute-sewing tools at our disposal. Now, we have to use them.

What Can Individuals Do?

What should employees do if they don’t live in a state that is pursuing a retirement strategy? All employees should explicitly ask their employers if they offer a retirement plan.

There are several options currently available to even small employers that will help employees and also provide for tax and retirement savings for employers. And, don’t forget to ask that auto-enrollment and auto-escalation be included in the plan.

It is also worthwhile to encourage state legislators in Arkansas and Mississippi to follow the lead of some other states and provide a state solution.

In Arkansas, a bill put forward in the 2017 legislaturewould have started us on the path to easier workplace savings for employers and employees in the form of a multiple employer plan (MEP). This bill was a great first step and a good conversation starter, but it stalled in the state Senate. So far, there have been no similar bills filed in Mississippi.

Retirement policy experts suggest that states offer a fully-hybrid model that combines marketplaces, open MEPs, and auto-IRAs. This model would provide better opportunities for access for all employees while offering employers a choice of how to offer a plan. “Employer(s) can choose to provide a qualified, vetted plan in the marketplace or offer an ERISA-based plan through an open MEP where the state serves as plan sponsor and fiduciary. Both of these options support employers’ ability to make contributions to their employees’ savings plans. However, if employers choose not to participate in one of these two options, the hybrid model requires they offer coverage through auto-IRAs. While auto-IRA plans do not allow for employer contributions due to limitations of the EmployeeRetirementIncomeSecurityAct, they use auto-enrollment and (in some plans) auto-escalation to support workers’ need to accumulate retirement savings.”

While states experiment, it’s also important to think nationally, too.

What Support Can the Federal Government Provide?

The Obama Administration began a federal retirement initiative with the myRA program, which was “an individual retirement account in which earnings and withdrawals [were] tax-free under certain circumstances—that invest[ed] in a U.S. Treasury retirement security which [was] guaranteed to never lose dollar value…. the myRA ha[d] no fees and… no minimum balance or contribution (deposit) requirements.” Unfortunately, the U.S. Department of the Treasury recently decided to phase out the myRA program; a Government review of the program showed that the program had too few enrollees to be profitable.

Even with the demise of the myRA, there is still an important role for the federal government to play in helping craft our parachutes. One idea being floated is that of a Guaranteed Retirement Account, a “mandatory, professionally managed accounts that supplement Social Security.” These accounts would be managed by the federal government and the retirement savings in them would be shared by employers and employees; they would split contributions equal to 3% of annual salaries. These accounts could bridge the gap between Social Security and retirement needs.

We have needles and thread and strong fabric at our disposal. It’s time to start stitching. No one should have to jump off the cliff without a parachute.

[1]Data Source: The New School Schwartz Center for Economic Policy Analysis (SCEPA) Retirement Equity Lab (ReLab)’s calculations from the 2014 Survey of Income and Program Participation (SIPP).

[2]A discussion of home assets and their value would not be complete without addressing the losses in housing values after the collapse of the bubble. While those with assets are still better off, values declined substantially. And, values are slower to rebound in less affluent communities, furthering the wealth gap.

[3]Historically, “teaching and other public-sector jobs were a ticket to the middle class for many black and female workers, who gravitated toward jobs with secure pensionseven if they paid for these benefits directly or indirectly through lower salaries. As a result, the share of black seniors receiving public-sector pension benefits is nearly as high as the share of non-Hispanic white seniors, and the share of female seniors receiving these benefits is almost as high as the share of male seniors.”

[4]Data for the chart comes from: http://www.economicpolicyresearch.org/images/docs/research/retirement_security/States_of_Reform_FINAL.pdf