This is National Save for Retirement Week, a national effort to increase personal financial literacy and raise public awareness about the importance of saving for retirement.[1] This week provides an opportunity for employees to reflect on their personal retirement goals and determine if they are on target to reach those goals. Southern Bancorp believes that building net worth is one of the best ways to ensure a strong financial future, which is why we’re so big on promoting the benefits of getting started saving for retirement now.

Of course, this is easier said than done.

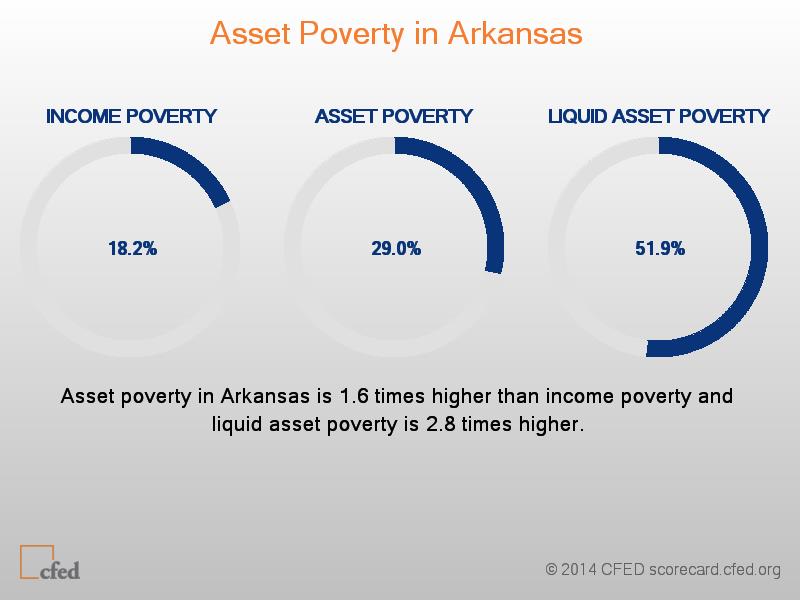

Research shows Arkansans and Mississippians are not saving at high rates, let alone adequately saving for retirement. According to CFED, the asset poverty rate is defined as the percentage of households without sufficient net worth to subsist at the poverty level for three months in the absence of income, whereas liquid asset poverty is not having sufficient liquid assets, such as cash in bank accounts and equity in stocks, mutual funds and retirement accounts, to subsist at the poverty level for three months. Arkansans and Mississippians do not fare well in either category, indicating most households are not appropriately saving for retirement.

A contributing problem for many folks in Arkansas and Mississippi is they simply don’t have the opportunity to save in a tax-sheltered retirement account because they lack access to a 401(k). In fact, according to the Employee Benefit Research Institute, only 39.2 percent of Arkansas workers and 41.4 percent of Mississippi workers ages 21-64 participate in an employer-based retirement plan.[2]

Today, a retiree beneficiary turning 65 can expect Social Security to replace approximately 30 percent to 50 percent of preretirement income, depending upon his or her earnings history. Consequently, if workers hope to maintain their preretirement standard of living, they may need other sources of income in retirement to supplement their Social Security benefits, as Social Security was not designed to match that standard for all workers.[3] Thus, saving for retirement is imperative to the future economic security of one’s family. With longer life expectancies and rising costs, it is critical that Arkansans and Mississippians understand the consequences of the need for and benefits of saving for their future.

Today, a retiree beneficiary turning 65 can expect Social Security to replace approximately 30 percent to 50 percent of preretirement income, depending upon his or her earnings history. Consequently, if workers hope to maintain their preretirement standard of living, they may need other sources of income in retirement to supplement their Social Security benefits, as Social Security was not designed to match that standard for all workers.[3] Thus, saving for retirement is imperative to the future economic security of one’s family. With longer life expectancies and rising costs, it is critical that Arkansans and Mississippians understand the consequences of the need for and benefits of saving for their future.

So what should one do to save for retirement if he or she doesn’t have the option to save in an employer-based retirement plan? There are several options at different levels:

- Individual: Even if one does not have access to a 401(k) plan, an individual can use a variety of different savings vehicles to prepare for retirement. The IRS provides a detailed list of all types of retirement plans here.

- State policy: While states cannot mandate that every employer offer a 401(k) plan, they can support increased savings through other means. Presently, Illinois State Senator Daniel Biss is working on legislation to provide automatic IRAs to workers earning $30,000-$100,000 annually that do not have access to an employer-based retirement plan. Arkansas and Mississippi could each consider introducing similar bills in their upcoming legislative sessions.

- Federal policy: In late 2014, the U.S. Department of the Treasury will begin offering myRA to help with financial stability during retirement.

Retirement savings is an important part of the larger financial strength picture. At Southern, we’re working to find unique ways to help families create economic opportunity, and ensuring a sound financial retirement is a good place to start for many.

For upcoming webinars and previously recorded webinars on saving for retirement, please visit http://www.icmarc.org/retirement-week/webinars.html. To learn more about Southern’s efforts to create economic opportunity in rural areas, please contact Meredith Covington, Policy & Communications Manager, at meredith.covington@southernpartners.org.

[1] Senators Gordon Smith (R-OR) and Kent Conrad (D-ND) established National Save for Retirement Week in 2006. It’s held every year during the third week of October.

[2] The participation rate increases for full-time, full-year wage and salary workers – up to 47.6 percent for Arkansas, 50.4 percent for Mississippi.

[3] Copeland, Craig. (2012). Employment-based retirement plan participation: Geographic differences and trends. Employee Benefit Research Institute. Available at http://www.ebri.org/pdf/briefspdf/EBRI_IB_011-13.No392.Particip.pdf.